disclosure in accord with the tcfd recommendations | sustainability | konoike transport-九州现金网

introduction

the konoike group recognizes that climate change is an important issue affecting the global environment, humanity, and corporate activities, and is actively promoting activities to mitigate global warming in order to contribute to the realization of a sustainable and prosperous society. the corporate governance code, revised in june 2021, recommends that companies listed on the prime market should disclose information in accordance with international frameworks such as the task force on climate-related financial disclosures (tcfd). in response, we work to enhance information disclosure on the impact of climate-change-related risks and opportunities on our business activities, etc., based on this framework. the details are as follows. the konoike group endorses the intent of the final report: recommendations of the task force on climate-related financial disclosures .

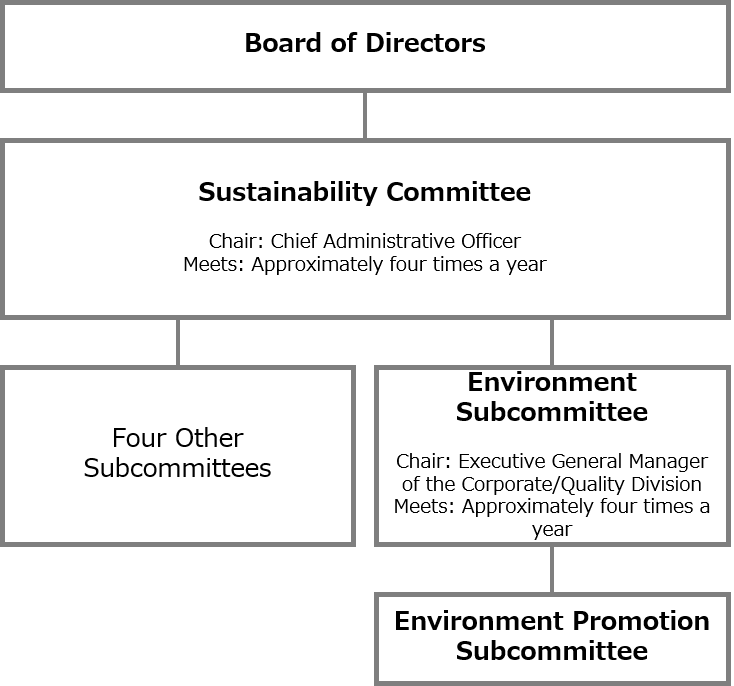

1.governance

- the sustainability committee has been established as an advisory body to the board of directors, and in addition to responding to inquiries from the board, discusses individual sustainability issues, including matters related to climate change, and reports regularly to the board on the content of these discussions.

- the environmental subcommittee shares information on the status of environmental initiatives at each headquarters every quarter based on environmental data from these headquarters, and discusses specific solutions for each issue. in addition, one outside expert is invited to the subcommittee to ensure fairness and objectivity.

2.strategy

(1) climate-related risks and opportunities

| category | impact | timeline | action policy | ||

|---|---|---|---|---|---|

| risk | transition | policies and regulations | possibility of worsening business performance due to increased tax burden associated with the introduction of carbon tax, etc. | medium-term | we plan to switch all electricity used at our locations to renewable energy by march 31, 2025. in addition, we will continue efforts reduce per-unit emissions by improving operational efficiency and introducing low-carbon technologies |

| technology | policy changes and stricter laws and regulations may increase the need to introduce new technologies that contribute to low-carbon emissions and/or increase the cost of replacing or installing new facilities | short/medium-term |

|

||

| physical | acute | increasing number of disasters caused by climate change, such as typhoons and river flooding, could damage our locations and jeopardize business continuity | long-term | we are evolving our business continuity plan (bcp: construction for disaster response, relocation, power and water outage countermeasures, etc.) | |

| chronic | potential deterioration in productivity and hiring difficulty due to hot working environments caused by rising temperatures | long-term | taking measures to reduce workload in hot environments (e.g., cool air blowers, neck coolers) to maintain occupational health and at the same time promoting labor savings through the introduction of technology and dx | ||

| opportunity | resource efficiency | potential to expand business opportunities through better pitching to customers by strengthening environmental measures such as co |

short/medium-term | improving operational efficiency and productivity in manufacturing and service provision processes, promoting modal shifts and joint delivery, etc. | |

| new markets | potential to enter business domains and areas where market expansion is foreseeable in a society with progressive co |

short/medium-term | we will work to identify growth areas in each industry and gather information and expand management resources to capture opportunities | ||

(2) scenario analysis

a. scenario analysis (qualitative)

the konoike group analyzed potential risks and opportunities facing the group in two scenarios: one in which temperatures increase approximately 2℃ (1.5℃) compared to pre-industrial revolution temperatures due to progress in global decarbonization efforts, and the other in which temperatures rise 4℃ or more due to no progress in these efforts. we analyzed impacts (risks and opportunities) of these two scenarios based on group-wide, function-specific, and industry-specific factors. in addition, we consider the direction of actions necessary for sustainable business in either of the two scenarios in our action policy.

(overview)

- group-wide factors consider important matters such as disaster risk at our own sites as well as co2 emission reduction measures related to logistics-related and environment-related recycling that emit high levels of co2. failure to address these issues may result in reduced business with customers, whereas if handled appropriately, may lead to increased business opportunities. as such, we consider these to be the most important factors to focus on.

- specific factors are divided into two categories: logistics-related and contracting-related. during customer supply chain disruptions, it is key to forecast and grasp their increasing outsourcing needs. these needs include improving operational efficiency and introducing low-carbon vehicles in logistics-related, improving productivity, and thereby reducing waste in the manufacturing process, as well as introducing equipment that contributes to low carbon emissions in contracting-related.

- other industry-specific factors are noted in the table below.

| category | 2℃ (1.5℃) scenario | 4℃ scenario | action policy | |

|---|---|---|---|---|

| (notes) | assumes a world in which ghg emission are reduced and rising temperatures are controlled (i.e., mainly transition risks surface). [major events and assumptions]

|

a world in which current business continues as usual (bau) and no measures are taken to reduce ghg emissions (i.e., mainly physical risks materialize) [major events and assumptions]

|

policies on how the konoike group will reduce risks and seize opportunities considering what would happen in either the 2℃ or the 4℃ scenarios. | |

| group-wide factors | [risks]

|

[risks]

|

[2℃]

|

|

| special factors by functions | logistics-related | [risks]

|

[risks]

|

[2℃ and 4℃] reduce energy consumption by improving operational efficiency (loading efficiency, actual vehicle rate, and actual operation rate). acquire capital resources through opportunities such as for modal shift and reverse logistics, establish a system to introduce next-generation technologies low-carbon as they become widely available. work to maintain and build partnerships with customers to partially collect on revised installation costs in the diffusion phase of next-generation technologies. |

| production and contracting services-related | [risks and opportunities] introduction of low-carbon technologies in production facilities (increased costs but appeals to customers) |

[risks and opportunities] decline in productivity and increase in difficulty of recruitment due to worsening of hot climates. increase in customer demand for outsourcing. |

[2℃]

|

|

| special factors by industry | steel-related | [opportunities]

|

[risks] negative impacts on operations due to water shortages caused by rising temperatures |

[2℃] deepen our involvement in acquiring work related to electric arc furnace steelmaking, as we have not worked much with it previously. maintain a system that enables us to continue undertaking blast furnace-related work over the long-term after we achieve hydrogen-reduced steelmaking. |

| engineering-related | [risks]

|

[risks]

|

[2℃]

|

|

| food | [risks] stricter cfc emission regulations and increased equipment replacement costs |

[risks]

|

[2℃] generally the same as group-wide factors. aim to expand business opportunities with customers by improving operational efficiency and switching to low-carbon vehicles in logistics-related while streamlining production processes and introducing production equipment that contributes to low carbon emissions (reducing waste) in contracting-related. |

|

| food products | [risks]

|

[2℃] generally the same as group-wide factors. aim to expand business opportunities with customers by improving operational efficiency and switching to low-carbon vehicles in logistics-related while streamlining production processes and introducing production equipment that contributes to low carbon emissions (reducing waste) in contracting-related. |

||

| life-related business | [opportunities]

|

[opportunities] increase in demand for hvac equipment due to rising temperatures |

[2℃] expand installation services (in-house use and external sales) of solar power generation and other energy-saving equipment, mainly through the techno service osaka and soka offices. seize business opportunities for clean energy in manufacturing and transportation. |

|

| medical-related | [opportunities] increase in equipment and materials, as well as their handling, due to the recycling and reuse of disposable medical equipment and materials, etc. |

[opportunities] increase in disasters → potential expansion in supplies and services for disaster relief |

[2℃] utilize the momentum for resource conservation and recycling to promote development of services and other areas for expanding the range of commercial products we handle. |

|

| airport-related business | [risks]

|

[risks] impact on human resource securement due to deteriorating working environments from rising temperatures and frequent extreme weather events |

[2℃] establish an efficient operation system and improve working environments by introducing decarbonized vehicles and promoting automated and unmanned vehicles, reflecting the infrastructure development policies and plans of each airport. |

|

b. scenario analysis (quantitative)

the konoike group estimated the impact amount of the carbon tax on the risks and opportunities identified in table (1) above by referencing the world energy outlook 2021 of the international energy agency (iea). please note that this analysis only provides general ideas in attempts to make a rough estimate of initiatives possible at this time. other risks and opportunities may also have positive or negative impacts. however, information for our analysis is insufficient at this time, and we have not yet been able to quantitatively calculate impact amounts.

carbon tax impact analysis results

| cases considered | 2030 | 2050 | ||

|---|---|---|---|---|

| impact amount | profit margin impact | impact amount | profit margin impact | |

| ① no efforts taken (bau) | -¥3,300 to ¥4,400 million | -0.8 to 1.0pt | -¥8,000-¥12,600 million | -1.3 to 2.0pt |

| ② 100% renewable energy achieved | -¥2,800 to ¥3,700 million | -0.7 to 0.9pt | -¥6,700 to ¥10,600 million | -1.1 to 1.7pt |

| ③ group goals achieved | -¥1,500 to ¥1,900 million | -0.3 to 0.4pt | no negative impact | |

| (reference) | ||||

| ②-① | ¥500 to ¥700 million | 0.1pt | ¥1,300 to ¥5,000 million | 0.2 to 0.3pt |

| ③-① | ¥1,800 to ¥2,500 million | 0.5 to 0.6pt | ¥8,000 to ¥12,600 million | 1.3 to 2.0pt |

(note) these figures were calculated based on the following assumptions by multiplying expected co2 emissions for each year by the carbon prices in reference 2. actual impact amounts will naturally vary depending on the design of the carbon tax (if combined with a corporate tax reduction, etc.). the above figures therefore represent rough indications of the extent of impacts on certain assumed business scales.

(reference 1) description of each case

| cases considered | details |

|---|---|

| ① no efforts taken (bau) | in this case, fy3/2022 emission intensities remain roughly the same as in 2030 and 2050 |

| ② 100% renewable energy achieved | in this case, emission intensities for 2030 and 2050 assume the successful and complete conversion to renewable energy, as planned in our next medium-term management plan |

| ③ group goals achieved | this case assumed group goals (2030: 35% reduction (vs. fy3/2019), 2050: carbon neutral) are achieved |

(reference 2) carbon price assumptions

(unit: yen/t-co2)

| assumptions | 2030 | 2040 | 2050 |

|---|---|---|---|

| sds*1 | 11,500 | 16,100 | 18,400 |

| nze*2 | 14,950 | 23,575 | 28,750 |

- sustainable development scenario: a scenario in which temperatures rise no more than 2.0℃ from before the industrial revolution, as set in weo2021

- net zero emissions by 2050 scenario: a scenario in which temperatures rise no more than 1.5℃ from before the industrial revolution, as set in weo2021

(注)(note) all carbon prices under the other advanced nations sections were converted at 1usd = 115 yen

(reference 3) 2030/2050 results and co2 emission assumptions

- figures for 2030 are based on our new 2030 vision. 2050 figures assume that sales will continue to grow at an annual rate of 2% from 2030 and calculated profit/loss to be the same as the 2030 profit margin.

- 2030 and 2050 co2 emissions were calculated based on the assumptions for each case in reference 1.

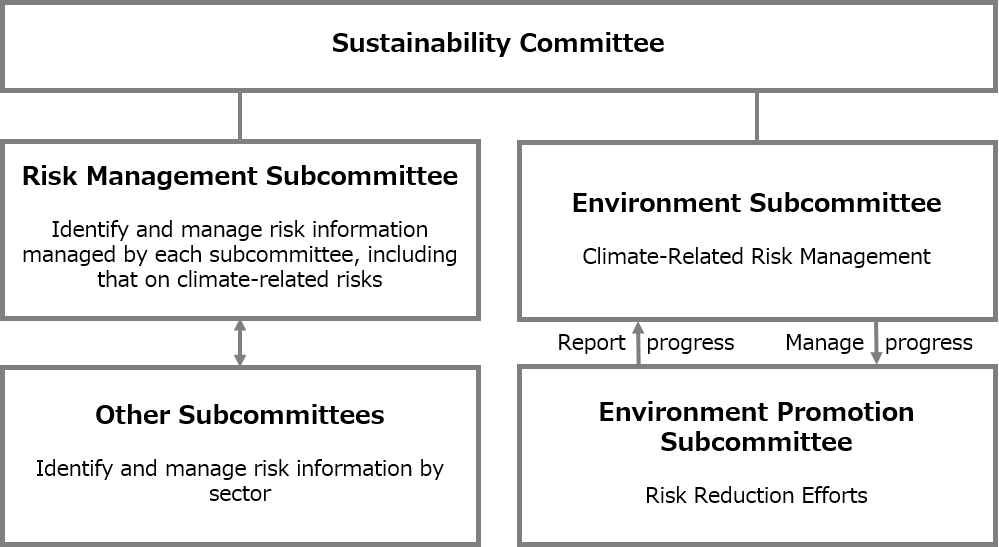

3.risk management

- information on group-wide risks is obtained and managed by the environment subcommittee for climate-related risks, and by the risk management subcommittee (chaired by the executive general manager of the general affairs division) for other risks by consolidating information from the various subcommittees.

- the environmental promotion subcommittee, which is under the environment subcommittee, continuously mitigates, identifies, and updates climate-related risks, and reports this content to the environment subcommittee, and then to the risk management subcommittee.

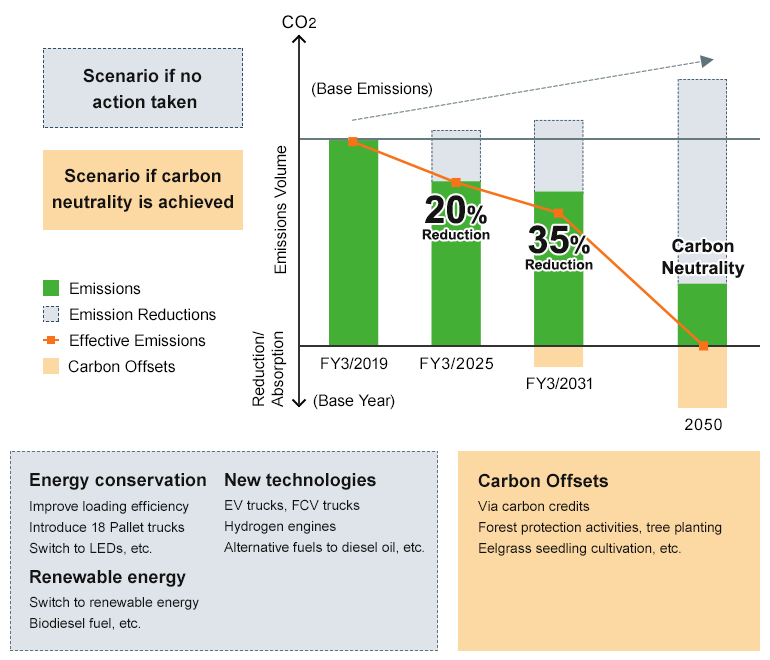

4.indicators and targets

・co2 emission reduction targets

| date | target | eligible entities | scope |

|---|---|---|---|

| 2025 (fy3/2025) | 20% reduction (vs. fy3/2019) | the non-consolidated company and domestic consolidated companies | scope1 and scope 2 |

| 2030 | 35% reduction (vs. fy3/2019) | ||

| 2050 | targeting carbon neutrality | ||

・efforts to achieve goals

to achieve carbon neutrality, we aim to reach 100% renewable energy use by march 31, 2025. in addition, we will also work to reduce co

・overview of co2 emissions reduction

the materials and information provided in this report include forward-looking statements. these statements are based on current estimates, forecasts, and assumptions that accompany risks and are subject to uncertainties that could cause actual results to differ substantially. risks and uncertainties include general industry and market conditions, as well as general national and international economic conditions such as fluctuations in interest rates and currency exchange rates. we are under no obligation to update or revise the forward-looking statements contained in this report, even if new information or future events arise.